We run equity and futures options financial trading strategies in multiple accounts for strategy diversification, as well as the usual asset diversification. This is a different discipline from our portfolio management approach, and actively traded accounts should definitely be separated from our long term hedged portfolio management accounts.

Our day job compliance restrictions require holding most financial instruments for total of 30 day calendar days, but they can be traded on the 31st calendar day. Specifically for options this means:

1) Must hold all option legs for minimum of 30 calendar days inclusive, and

2) Must not trade on any option positions with less than 30 calendar days to expiration.

Obviously this determines the trading strategies that we can employ. Briefly we would define a Trading Strategy as taking short or medium term (1 day to 3month ) direction bets (long or short) with limited risk (stop loss only risking 1% of account per trade) relative to the total account size (e.g. 100k).

Trading Plan for 30 day trading option strategy

In order to run a strategy trading there needs to be have defined set of rules to keep you in business over a period of several years. Trade equity options in two IRAs to reduce tax implications, and trade future options in standard margin account. These rules are the template to trade equity and futures options with a 30 day rule.

Please note: These rules can still be applied to any trading strategy without a 30 day rule, so just because you do not have these restrictions does not mean it cannot be useful for your trading.

Entry Rules

Trade Small

1% of account max risk per trade. If account $10k, only risk $100 per trade. Need to be careful of commissions when trading this small as some strategies will not be viable with only 1 to 2 contracts. If account size increases (or decreases) should size trades accordingly.

Initially focus on ETFs with penny wide option pricing only. This is a surprising small of about 35 ETFs – see below:

DIA EEM EFA EWJ EWT EWW EWY EWZ FXE FXI GDX GLD IWM IYR KRE QQQ SLV SPY TLT UNG USO UUP VXX XHB XLB XLE XLF XLI XLK XLP XLU XLV XLY XME XRT

When doing:

– bull put or bear call credit spreads, IV RANK must be greater than 35, with at least 60% chance of expiring worthless

– iron condors, IV RANK must be greater than 35, with at least 70% chance of expiring worthless.

– atm 50/50 debit call or put spreads ideally IV RANK should be less than 25, or trade is entered for about half width of the strike (eg only pay $0.50 for a $1 wide spread)

– trading straddles it is better to buy junk options longer term in same expiration month, than near term month options (eg better to do every leg 45 days out, instead of buy protection junk wings 30 days out, then sell 45 days out). Note: this doesn’t really provide “protection” but in extreme moves it limits max loss, but doesn’t significantly reduce return on capital. Importantly this also makes straddles IRA eligible.

Trade Often

40 to 60 calendar days to expiration, sweet spot is about 45 days to expiration. Use weekly option chains if necessary. Try and avoid trades that have only 1 week or less to expiration AFTER 30 day holding period has elapsed. This avoids unnecessary gamma risk closer to expiration, and typically makes the trade move “slower” the further is it from expiration.

ALWAYS use mid price limit order plus or minus $0.05 (depending on direction) then cancel and correct in $0.01 increments for immediate execution.

Alternatively just hang out a DAY limit order at your target price. Don’t use GTC unless you are disciplined and remember to cancel so it does not fill with less than 30 days to go to expiration.

Generally don’t sell an individual option leg with a premium less than an absolute value of $0.20. This due to the percentage of the trade that goes towards commissions getting in and out. Eg on a 1 lot would be $20 credit minus $7 in and $7 out leaving little room for profit.

Set calendar pop up or alert for morning of tradable window and expiration Friday to make sure no positions will be assigned

Trade exit

Exit if greater than 50% max profit

Trade uncorrelated

Compare new trades probable asset class correlation to rest of portfolio.

Enter the proposed ticker with each other porfolio ticker. If the correlations are above positive +0.5 for more than half of the time on the graph with any other ticker try not to include or trade smaller than usual. Temporary spikes over +0.5 are ok, but not consistent.

| Correlation | Description | Diversification Benefit |

|---|---|---|

| -0.65 | Asset pair with negative correlation | Excellent Diversification |

| -0.15 | Asset pair with slight negative correlation | Good Diversification |

| 0.2 | Asset pair with mild positive correlation | Moderate Diversification |

| 0.8 | Asset pair with strong positive correlation | Poor Diversification |

Exit Rules

Check 30 day rule on ALL OPTION LEGS

Always double check 30 day date on position in brokerage acct before trading to exit (calendar entries can be wrong). Enter that TD in 30 day spreadsheet to make sure that exit date is exactly 30 calendar days after original trade date. A quick reference is if the entry trade date (TD) month has:

31 days, then exit TD is 1 day less than entry TD

30 days, then exit TD is same as entry TD

29 days, then exit TD is 1 more than entry TD

28 days, then exit TD is 2 more than entry TD

Place Outlook calendar updates in advance for trade exit date when entering trade (e.g. “Trades – Sept 25th 2015 1) Exit IWM butterfly 2) Close SPY Sept/Oct calendar”)

Profit taking

Based on % of max profit

If at less than 50% of max profit, then exit immediately

If more than 50% chance (according to option probabilities) of making a profit between now and expiration – hold the position and reevaluate everyday between now and expiration.

If less than 50% chance of making profit, eg through a short strike, look to

– exit and do not re-establish OR

– roll entire position to next month immediately OR

– exit half position and hold for a few more trading days to see if can recover to break even.

Trade Risk not unrealised profit/loss

Trade risk on outstanding position, not existing p/l. See Stock twits podcast called Take exits, not profits

Examples

Ewz bull call spread $36.40 dec 23rd

Jan 30th 2015 long 4 call contracts $36

Jan 30th 2015 short 4 call contracts $37

Cost basis: $0.54 (filled at 0.50 & commissions)

Max risk: $216 if EWZ under $36 by expiration

Max gain: $184 if EWZ over $37 by expiration

XOP covered strangle trade for efficient use of capital – May 2015

Long May 15 2015 $35 call

Long May 15 2015 $35 put

Short May 15 2015 $45 put

Short May 15 2015 $50 call

Requires about $1000 in margin, instead of $4800 (approx) to buy stock – better ROC

Trading Adjustments for 30 day rule – same month

Typically it is better to use limited risk reward strategies and let the original option probabilities play out over the full trade life cycle, rather than trying to adjust the trade significantly along the way. There are some trades where adjustments that can be made, but they always need to make sure that those new option legs can also be held for 30 days.

Usually if the iron condor was placed for a 2 or 3 point wide in an index ETF, then the risk/reward was established on order entry, so you wouldnt want to adjust it. You typically only try and adjustment with delta hedge significantly when :

1) there is a huge market move (like Jan 2016) or

2) when you have lots of similarly correlated positions on in the same account. For example, all your iron condors in IWM, SPY, QQQ are getting hit at the same time.

3) the original iron condor was quite wide and you didn’t think it would get hit. For example, risk $500 to make $100, 5:1 risk/reward, versus the usual 3:1 risk/reward iron condor.

An adjustment is to an original trade is usually only made when a massively different directional assumption is required. A recent example would during the Jan 2016 sell off, selling call spreads against positions to reduce long delta. Many neutral strategies (such as iron condors) were started in Dec 2015, but became net long due to running through the short put spread in the iron condor. This caused a neutral assumption to become bullish, in a heavy down market. Therefore short call spreads were sparely used to offset the (unwanted) bullish positions.

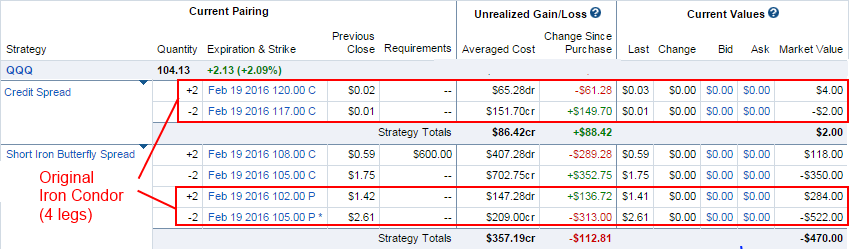

For example, this an 3 point wide iron condor on QQQ that was started on 31st Dec 2015 (50 DTE). This trade had a max profit of $150, with a max loss $450:

max loss = (width of strikes x contract size x 100 – credit received) = 3 x 2 x 100 – 150 = $450

This required playing defensive on an iron condor which went immediately against our position touching the short 105 put, but could not be exited due to the 30 day rule.

The important part to note is the number of days to expiration (DTE) was less than 30, so the position could be adjusted by applying an ATM call spread. The implied volatility was high in the sell off, so selling an ATM call spread gave some decent premium on the spread.

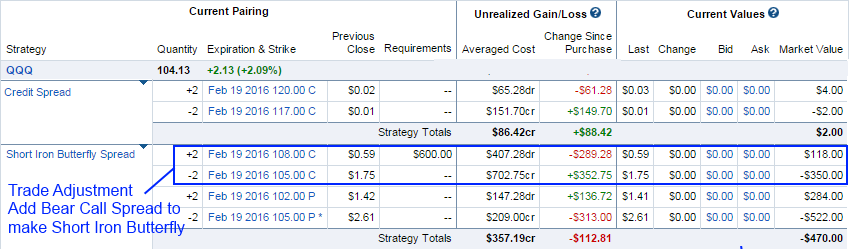

Then adjusted to a short iron butterfly on by adding the bear call spread on 7th Jan 2016 (42 DTE) – highlighted in blue:

This adjustment added a further $295 in credit, meaning that the max loss is now $450 – $295 = $155. This has effectively greatly reduced the risk on the iron condor. This trade will make most money if QQQ expires at 105 in Feb 19th 2016 expiration – however it that would need to pin the strike very closely, so a more likely explanation is that it is a small loser if it finishing outside the $102 to $108 range in either direction by Feb expiration.

The market was significantly less volatile when the trade was placed, and in an environment of high implied volatility and daily downward markets, this was a nice way to neutralize the trade without it out for 30 days.

However this was only possible because there was 30 days to go expiration. The next section describes what to do if there is less than 30 days to go expiration

Trading Adjustments for 30 day rule – next month

Important note: Adjustments to limited risk reward trades (like iron condors) with less than 30 days should only be made with caution. This is because the option premium can often bounce back if the market has gone strongly in one direction. You can end up with positions in multiple months, where the 2nd month has to be held for 30 days after the near month position has been exited. This can mean having market risk on that you wouldn’t normally construct a trade in the 2nd month For example, if you started with a neutral market assumption in the near month, and then added a call spread in the 2nd month, when the near month iron condor is exited (neutral trade) you automatically have a bearish call spread in place which then may have to be held for 20 days. In summary you have to be comfortable keeping the 2nd month trade adjustment on, after the near month trade has been exited. It is therefore not a good idea to add trade adjustments with poor/risk reward in their own right (e.g. call spread max profit $100, max loss $900) just to reduce the risk on the original near month trade.

To be clear the objective of the adjustment to an iron condor is to try and make the trade close to a scratch (not lose any money at all on it) even if you have to hold the position for a month or so. You are not likely to make money from an adjusted iron condor, if you can get out for even money after adjusting you should be happy and move on to the next trade.

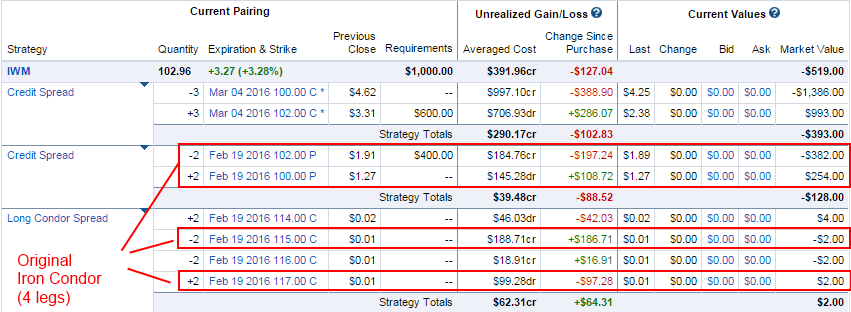

For example, this an 2 point wide iron condor on IWM that was started on 5th Jan Jan 2015 (45 DTE). This trade had a max profit of $128, with a max loss $272:

max loss = (width of strikes x contract size x 100 – credit received) = 2 x 2 x 100 – 128 = $272

This screenshot highlights the original iron condor 102/105/115/117:

Again this required playing defensive on an iron condor which went immediately against our position touching the short 102 put, but could not be exited due to the 30 day rule AND for the 2nd adjustment there was less than 30 days to go to expiration.

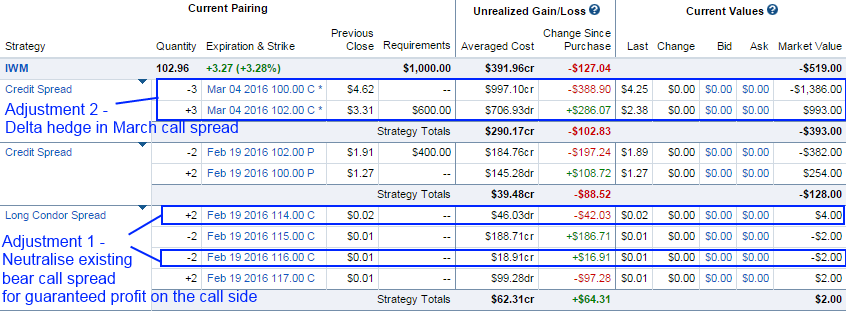

The 1st adjustment was done on 11th Jan 2016 to lock in a minimum gain of $62, but only on the call spread part of the iron condor. This can be left to expire into Feb expiration, because it has a minimum gain of $62 where ever IWM goes.

The 2nd adjustment was done to delta hedge the position when it went in the money and the rest of the portfolio had too many long deltas, so needed to apply short call spread to get some short deltas. However this was done on 21st Jan 2016 using March 4th 2016 weekly options. The trade adjustment needed to go out to March, because the trade date 21st Jan was less than 30 days out from the original trade expiration date of 19th Feb.

This screenshot highlights the two trade adjustments to the original iron condor:

Note: that if we had not adjusted, then the original iron condor 102/105/115/117 would be at breakeven as of 29th Jan 2016. The current position with all its adjustments is losing $127. However if the market had sold off significantly instead of rallying, then the March delta hedge would have done its job and mitigated the loss in the Feb options.

The important point to note is to learn how to delta hedge with the 30 day rule, not try and second guess where the market will go. Hindsight is always 20/20.

Trading Adjustments for 30 day rule – when NOT to adjust

As discussed previously, typically it is better to use limited risk reward strategies and let the original option probabilities play out over the full trade life cycle, rather than trying to adjust the trade significantly along the way. This is due to the direction of being whipsawed by the market – for example, a big down in market causing you to delta hedge with call spreads, then immediately follows a big up move in market the following next week – and your iron condors back making money again, except for your delta hedge adjust call spread which is now massively ITM and losing most of your iron condor profit! Hindsight is 20/20.

Every trade has a theoretical probability of profit when you place the trade, typically a 60% chance or more of making money at expiration for iron condors. Therefore presumably if you do enough of them you will (on balance win 60% of the time). So why not just adjustment every time when the market hits the short strike ? Because adding adjustments messes with the probabilities and sometimes even adds options in multiple expiration cycles. Therefore the original trade probabilities don’t hold anymore and its hard to accurately predict the probability of running 100 iron condors + your 100 random adjustments. Basically its just not the same trade any more – the initial trade entry option probabilities are only for a vanilla iron condors. If you fiddle with extra option legs, you’ve changed trade exposure to unpredictable things like the market volatility at near month expiration – for example if implied volatility is very high when you at near month expiration, your back month spread could just be breaking even; however if implied volatility was very low at near month expiration, your back month spread could have a nice profit – but its hard to predict in advance implied volatility in advance where trades span multiple months. This is why it can be hard to predict exactly the profitability of a Calendar spread, because when the trade is ATM close to expiration, the trade profitability can depend on higher implied volatility in the back month.

Next we can review our Trading Strategies

2 thoughts on “30 Day Trading Plan”