This trade adjustment on European based Bitcoin fund SE:BITCOIN.XBT describes reducing bitcoin exposure inside a “speculative” trading IRA. The main reasons for selling the bitcoin fund are portfolio rebalancing, mitigating long term provider risk and high product expense fees.

Portfolio Rebalancing

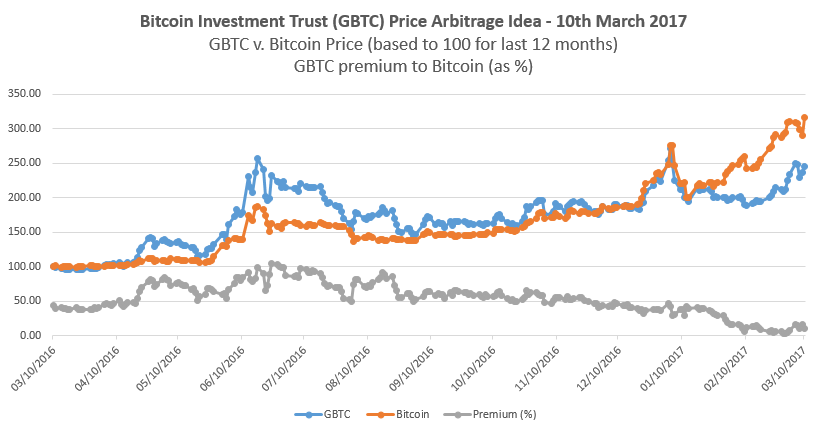

This trade has been a multi year Bitcoin long, trading two Bitcoin tracker fund products GBTC and SE:BITCOIN.XBT. Both funds aim to track the Bitcoin price (BTC), and own a claim on underlying Bitcoin. For brevity the underlying Bitcoin owned by either fund will be referred to as the Net Asset Value (“NAV”). As a quick review GBTC is Grayscale’s well known investment trust whose price is tied to Bitcoin. The initial GBTC position was originally purchased in March 2017 with BTC at $1,250 – see initial trade entry for more background.

However in 2018 due to GBTC having a very high premium to the actual underlying bitcoin holdings (NAV), it became very unattractive as a long term holding. Therefore the entire GBTC position was replaced with a more obscure Bitcoin fund SE:BITCOIN.XBT traded in Swedish Krona on the Swedish stock exchange. The fund historically tracks the Bitcoin price much more accurately than GBTC with only a nominal premium to NAV. Bloomberg has average 52 week trailing NAV of -0.12% for SE:BITCOIN.XBT, but a whooping 18.22% for GBTC (as of Feb 4th 2021). Incredibly around year end 2017 and into 2018 the average 52 week trailing NAV premium was 53% for GBTC (on 16th Feb 2018) and occasionally spiked over 90%.

GBTC was sold in Feb 2018 due to this huge premium to NAV – see the original trade exit for a detailed discussion. The final sale value contained NAV (the equivalent amount of Bitcoin held by the fund) and the premium (that the market assigned over fair market value for the Bitcoin held in the fund). The NAV amount was then reinvested into crypto with approximately two thirds in Bitcoin (SE:BITCOIN.XBT) and one third in Ethereum (SE:ETHEREUM.XBT). That maintained exactly the same amount of crypto holdings, but with some crypto diversification and greatly reduced exposure to fund premium. The premium part of the sale was “taking money off the table” and was invested into other portfolio assets. This crypto rebalancing trade was done at approximately BTC $10,025. All these trades were IRA eligible so rebalancing was not a taxable event. Rebalancing these XBT funds frequently would not be advised because of the wide trading spreads and international transaction fees.

Fast forward 3 years to Jan 2021. Crypto prices have gone through a huge decline (a “crypto winter”) from about Dec 2017 to Dec 2018 – with BTC ultimately reaching a low of $3,300 around Dec 2018. Then came the recovery rally from Dec 2018 to Sept 2020 with BTC reclaiming $10,000. Following that Bitcoin has been on a rocket ship launch starting in Oct 2020 at approximately $10,600 about to a high in early Jan 2021 of $40,405. The latest boom is claimed to be institutional money buying in large tranches, chasing exposure for themselves or their clients.

In Feb 2018 felt like we hung around at the party too long, with BTC moving from a peak around $20,000 in Dec 2017 down to our rebalancing trade at $10,025. Were actually saved somewhat by being able to the capture the GBTC premium. So this time we decided to see if we can improve by selling near the top of a huge peak, not waiting for post peak decline (speculation of course). Therefore during decline from high in early Jan 2021, exited two thirds of Bitcoin SE:BITCOIN.XBT position on 20th Jan when BTC was approximately $35,105 (about 13% from peak a few days earlier).

Ethereum (SE:ETHEREUM.XBT) position was maintained with no reallocation. Even after allocation the speculative IRA portfolio still has 25% crypto exposure, of which approximately 60% is Bitcoin and 40% Ethereum.

Provider Risk and Fees

Any crypto exchange traded product (such as GBTC or SE:BITCOIN.XBT) has some significant counterparty risk if held for several years. Fund could get hacked, the provider may lose private keys or have some other internal company disaster that impacts the underlying crypto holdings. There is also significant provider discretion about how to handle hard forks and how (or whether) they accrue that value back to fund holders. Bluntly there is a constant tail risk that one day investors lose some or all of their investment in a crypto fund (potentially overnight with no warning). Ironically holding these crypto funds puts a single point of failure back on to the provider – that the underlying crypto “trustless” philosophy was supposed to resolve.

Both crypto funds have very high management fees that mimic hedge fund style management fees. GBTC has 2.0% management fee (but higher NAV premium) and SE:BITCOIN.XBT management fee 2.5% (0.5% higher, but less NAV premium). Although crypto funds may be able to justify high fees due to the very specialized product, this has to be a long term holding concern – especially given industry trend towards much lower fees. As any crypto fund position size grows, the management fee becomes much more expensive annually in absolute real $ amounts. Investor alternatives to paying crypto funds management fees are managing their own crypto keys in cold storage. Cold storage approach has no management fee, but requires investor have a detailed crypto knowledge of potential multiple cryptos. An investor needs to balance no management fee in cold storage, with the possibility losing their investment due to their own mismanagement. Therefore the fund management fee is an expensive convenience fee to trade crypto on exchange, manage crypto in cold storage and implement security protocols.

Investors can currently ignore high fees because crypto is currently trading on Fear Of Missing Out (FOMO) momentum – who cares about 2.5% fees when you make 300% plus per year? However through down markets over years or months, the fees begins chip away at long term value. The Nerdwallet Mutual Fund calculator can be used to compares product fees for an initial $10,000 investment in the (clearly hypothetical!) scenario where BTC price is static. Example shows that with no BTC price appreciation simply holding SE:BITCOIN.XBT with its 2.5% management fees loses nearly 12% in fees over 5 years – just for holding.

This clearly shows the impact of high management fees on long term holdings – these funds can only be held if high confidence crypto will rise. However as a medium term trading vehicle for crypto exposure with no taxable gains in an IRA, it is well worth these risks. Just remember to periodically take some off the table to mitigate the provider and management fee risks.

Summary

GBTC and SE:BITCOIN.XBT products are a good trading proxies for crypto, but are still third party representations of a “promise to pay”. If you don’t have your own private keys, you don’t truly own your crypto. Crypto funds should not be relied on for multiple year long term buy and hold crypto exposure. Only crypto in cold storage does that.

The crypto asset class is incredibly hard to hold without taking at least some money off the table on the highs. The peak to trough declines were about 85% for BTC and 94% for ETH from Dec 2017 peak to Dec 2018 trough. Unless some house money was already taken off the table in Feb 2018, it is doubtful that would have held all the way through “crypto winter” without finding the need to “do something”.

There is a reasonable chance that BTC goes significantly higher – however there are better asset classes that are less frothy starting from a lower base. BTC can potentially move from $35,000 to $100,000 from high (e.g. 200% return) but there are better opportunities to redeploy some of that crypto capital. Selling some for portfolio allocation is not the same as being bearish on crypto. This speculative IRA portfolio still has 25% crypto exposure, because it is the gift that keeps on giving. However if/when the crypto music stops, we will have made enough to construct an entire new portfolio from one single original Bitcoin position – whatever happens to BTC in future.