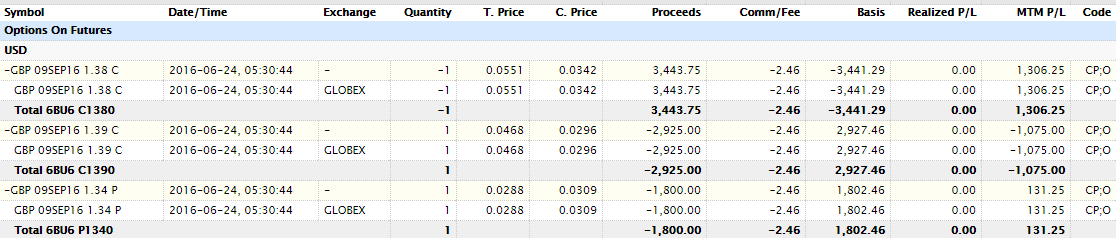

Despite threatening to breakout to new highs in August 2020, the gold price in July 2021 is actually about the same as one year previous in July 2020.

While the Gold price has moved around in a range for the last year, the volatility in the Gold market has been steadily declining this year. This steady decline in volatility is arguably surprising given all the macro economic fallout from the Covid stimulus and other economic measures. However the Gold market appears to be predicting less pronounced moves, at least in the short to medium term.

Since there is low gold volatility we can take more time premium risk than usual and keep the call strike relatively close to the money. Using deep in the money call options is a favorite strategy to get leverage to an underlying without taking the same principal risk as long stock. Buying in the money call options typically means that the majority of the option premium is intrinsic value (“real” value not time value). However the time value of an ITM call option can still be much cheaper when the underlying volatility is low. The spread will also benefit if Gold volatility increases during trade, which is a possibility given volatility tends to be mean reverting.

Gold LEAP diagonal spread

Therefore we can take advantage some of the lowest gold volatility this year, and buy a very long dated LEAP call for Jan 2023 (with a 66 delta). Buying 10 GLD options is approximately the same size as a single call option on a /GC futures contract (obviously assuming similar strikes and expiration dates).

To try and pay for some commissions on the larger trade and get a small amount of income, the shorted dated Sept 2021 $190 call option will be sold (7 delta). This option has a 93% chance of expiring worthless at Sept expiration (100 delta minus 7 delta). But also a 14% chance of being touched between now and expiration (“double the delta”). Using the shorter dated short call does chip away at the cost basis every month. However it does mean that would likely have to roll and re-evaluate position if GLD price shoots up more than 10% in a couple of months – from todays close price $171 to $190 in September.

As of close on July 14th this gives the spread a long delta of approximately 58 delta. The long dollar amount for 10 contracts gives about $99,180 equivalent gold exposure (specifically $171.04 GLD price x 1000 shares x 0.58 spread delta). The long call Jan 2023 call is $19.85 and the short Sept 2021 call was $0.42, giving a maximum risk is $19,430 until Jan 2023 in approximately 18 months time. The maximum risk amount is calculated by (long 10 contracts x 100 x $19.85) + (short -10 contracts x 100 x $0.42) = $19,850 – $420 = $19,430. However there is plenty of time to adjust between now and Jan 2023, so the likelihood of realizing the full loss is low.

|

|

Importantly if GLD goes over $180 the Jan 2023 $160 will over its breakeven price, and will begin to trade more like an underlying stock position as the option delta moves towards 100. The call option leverage allows paying less than $20k to control a $100k gold position. The long dated call also reduces the risk in a protracted gold sell off. Giving time to adjust and roll as conditions warrant (e.g. higher volatility) or gold price opinion changes (e.g. gold price declines and would like to exit to maintain some option value for other trades).

In summary this is a leveraged gold long position as a portfolio "hedge" to avoid "missing out" on a run away gold price. It gives plenty of time for the idea to play out. Additionally the capital efficiency of LEAP calls manages the downside risk, but gives a significant upside potential if Gold moves up in next 18 months.